The venture capital industry is increasingly being reorganized around "mega-funds," making it harder for small-scale innovative investing and new entrants to survive. Drawing on personal experience, the author methodically analyzes the "mechanical limits" of venture, the monotony of investment culture, and the shifting motivations behind entrepreneurship — arguing that the VC industry's future is no longer a promising path for young idealists. What remains is a handful of large funds wielding excessive capital and platform power, and a startup culture increasingly locked in place by their influence.

1. Between the Appeal and the Reality of Venture Capital

When the author enrolled at NYU Stern, venture capital was the one career that genuinely excited them. The process of identifying which company among the countless startups born each day would become "the king" — and the intellectual blend of philosophy, finance, technology, and world-building embedded in that process — held a powerful allure.

But three years later, after meeting countless founders and investors, the author found themselves still unable to grasp the "plot" of the VC industry. They put it plainly:

"There's something about the venture system I just can't make sense of. And my gut tells me the future isn't bright for emerging investors like me." 🌫️

2. Venture Doesn't Scale — The Numbers Make It Clear

The industry's defining axiom — that "venture doesn't scale" — is borne out by data. In 2018, the top 10% TVPI (total value to paid-in capital) for funds over $100 million was 1.67x, while funds in the $1M–$10M range returned 4.03x. Small funds outperformed by more than 2.5x.

The reason lies in venture's structural constraints. One investor explains it this way:

"To return 3x on a $5 billion fund, you'd need to hold over 10% of both Meta and Uber — the two greatest VC outcomes ever — from seed all the way to IPO. And that still wouldn't be enough."

On top of that, average seed ownership has shrunk to below 10%, and the time from investment to IPO has stretched to over 11 years. For large funds, generating legendary returns requires outcomes that border on the miraculous.

3. The Power Law and the Self-Fulfilling Structure of Mega-Funds

Some argue that venture is designed to chase exceptional outliers — the power law — but the reality falls short of that ideal. When an AI startup is valued at $120 million at Series A, every subsequent round demands justifying increasingly astronomical valuations. In practice, DPI (distributions to paid-in capital) and liquidity metrics are deteriorating across the board.

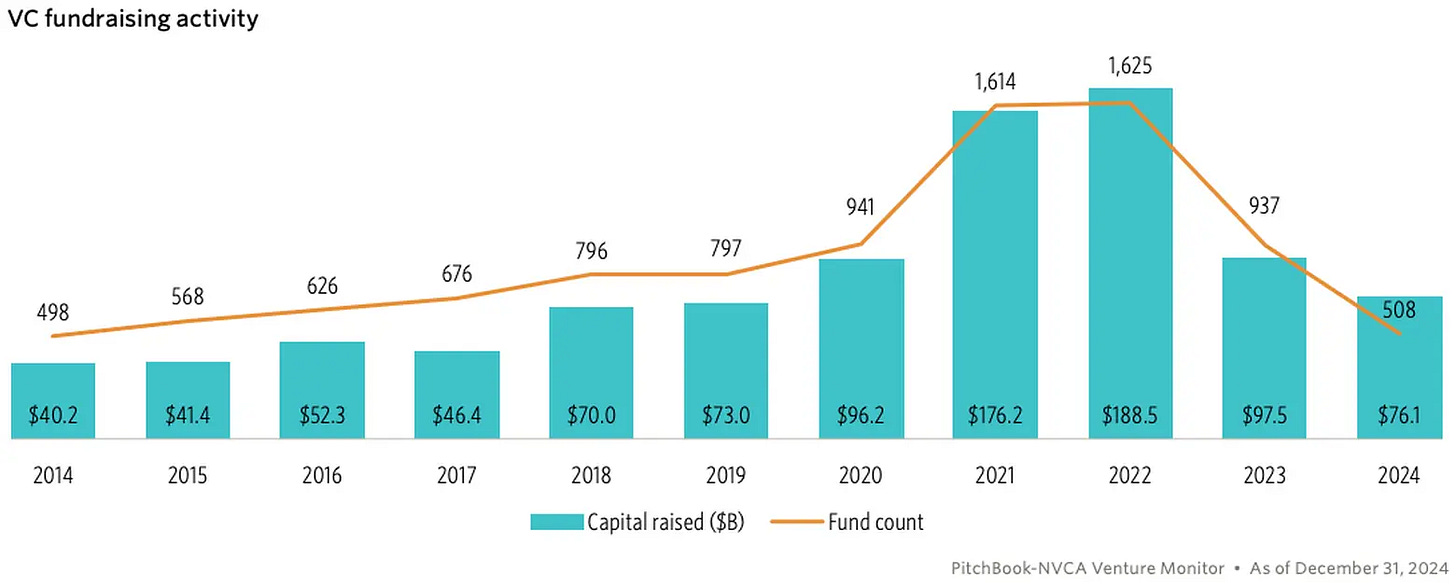

This is fueling growing frustration among Limited Partners (LPs). In 2024, only 508 new funds were formed — the lowest in a decade — and the total number of VC funds fell from 8,115 to 6,375 between 2021 and 2024. As capital return timelines lengthen, institutional money is flowing away from the VC market.

"Small funds and pioneering investors are fading out. Capital is concentrating in the mega-funds that have historically delivered the strongest results." 🏦

4. Capital Concentration in Mega-Funds and Its Effects

In 2024, the top 9 funds captured more than 50% of the $71 billion raised across the entire venture industry. The image below illustrates this structural shift visually.

Large funds move faster, offer better terms, and command powerful talent and networks (a16z, for example, employs over 428 people). As of 2025, the top 20 funds participate in more than half of all seed-to-Series A rounds of $10 million or more. They capture a dominant share of deals from the very beginning, leaving smaller VCs with ever less room to compete.

The logical endpoint for VC funds looks like this:

"Venture capital is no longer just about returns — it's become a meta-allocator that controls cap tables and chooses kings. Speed, access, and 'platform gravity' override everything else." 🚀

5. The Changing Culture of Entrepreneurship — The Loss of Motivation and the Rise of Mimetic Signaling

More broadly, shifts in how capital is deployed have had a significant effect on startup culture. The expansion of mega-funds has moved founder motivations away from original vision and toward winning validation from "name-brand investors," with social status and imitation becoming the primary drivers.

"The vibe of recent AI slop machines and YC batches is just exhaustion and hollowness. Founders who used to dream about the future now feel like they're building just to build."

A conversation with a Stanford student captures this starkly:

"I think getting into YC for résumé padding is easier now than landing at a big tech company or a quant firm."

The result: imitation and social status have displaced genuine innovation as the dominant motivation for founding companies. And that means it's not just the barriers to entry that have dropped — it's also become harder for truly extraordinary, landmark companies to emerge.

6. Rising Barriers to Founding and Funding Startups

The platform strategies of mega-funds add further structural friction for aspiring founders. Initiatives like YC's "Request for Startups" attract far more candidates than the market can actually support, stoking hyper-competition. Building a great software company has already reached something like a "completion stage." Market opportunities are finite, but the number of founders is growing exponentially.

"For individual founders, the market 'alpha' — excess returns — and the space of viable ideas have shrunk dramatically. The overall volume of innovation may be rising, but it's becoming an increasingly grueling market for each individual participant."

7. Other Signals of Change

Beyond the structural dynamics, the author intuitively detects several additional shifts:

- Incumbents moving at unprecedented speed and responsiveness Small startups once held an advantage in agility, but now companies like OpenAI, Meta, and Google reshape the landscape week by week.

- Continued compression of software margins The cost of building software is approaching zero, and strategies for extracting margin from legacy markets via technology are in vogue — but these require massive capital, which once again tilts the playing field toward mega-funds.

Closing: At the Crossroads of Growth and Decline in a New Era

The venture capital industry is entering a phase of maturity rather than growth. The author hasn't lost their affection for the field, but honestly acknowledges that making a meaningful impact within it is far harder than it used to be.

"A lot of people give up too early, but I think wrestling with these questions is actually what helps you find a genuine sense of direction for the future."

It's worth remembering that venture capital is no longer a growth stage for young innovators and nimble small-fund investors — it's transforming into a predictable game dominated by a small number of giant funds.

😊 Thank you for reading