1. Introduction: Crisis and Opportunity for AI Applications

In March 2025, OpenAI's upgraded 4o model was released, and the internet was instantly swept up in an image-generation frenzy. Users around the world remixed images in a variety of artistic styles — including Studio Ghibli — generating more than 700 million images in just one week.

"Users generated more than 700 million images in just one week."

This phenomenon instantly plunged leading image-generation companies like Midjourney into an existential crisis, with predictions that competitors would soon release similar capabilities. Foundation model companies, locked in fierce competition, were already going beyond image generation, releasing audio generation capabilities via API.

In this environment, a natural question arises:

"If foundation models offer similar functionality, do we really need specialized AI applications?"

2. Zero-Value Threshold: When an AI Application's Value Collapses to Zero

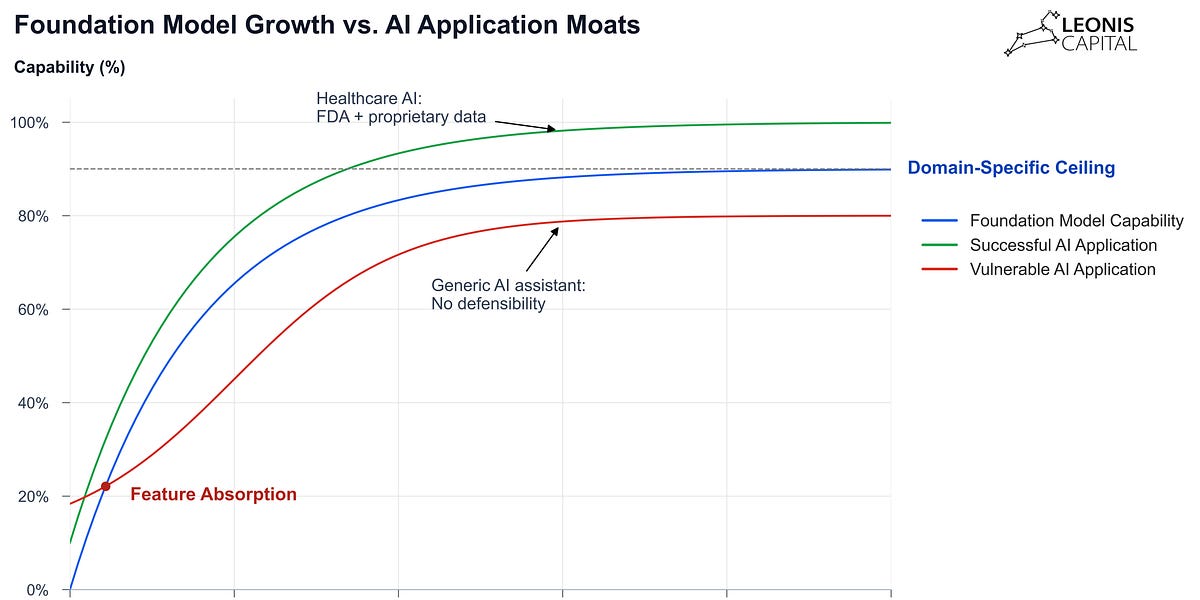

According to the "Zero-Value Threshold" principle introduced in Part I, once a foundation model or application crosses this threshold, its value collapses to zero almost instantly.

AI applications in particular are always exposed to the risk that their own platform — the foundation model — will absorb (cannibalize) their functionality. In practice, once a foundation model begins offering a new capability natively, formerly independent applications are repeatedly reduced to "just another feature" and disappear from the market.

"The moment a foundation model ships a new capability, the value of any application that provided only that capability drops to zero instantly."

3. The Dual Threat Facing AI Applications

AI application startups face two distinct threats:

-

Vertical threat: Foundation models directly integrate core application capabilities — such as image generation or domain-specific reasoning.

-

Horizontal threat: Other application startups rapidly replicate features and enter the market.

"As the cost of code approaches zero, feature replication becomes easier, and a single capability alone can no longer form a defensible moat."

4. The Absorption Pattern and the AI Startup Collapse Cycle

AI startups initially attract attention with novel use cases (e.g., advanced summarization, specialized image styles), but soon a foundation model upgrade arrives that matches or surpasses those capabilities. At that point, users start asking:

"Do I really need a separate solution for this?"

Churn accelerates, and the application's value plummets. This has already played out at companies like Jasper, and the pace is only accelerating.

5. Real-Time Industry Examples

-

Coding agents: In March 2025, Anthropic released Claude Code, enabling even non-specialists to delegate coding tasks from the terminal using natural language. While it doesn't yet threaten specialized developer tools like Cursor, existing AI coding assistants are finding their position increasingly squeezed.

-

AI search: As foundation model companies — OpenAI, Grok, Google — rolled out their own search features, AI search applications like Perplexity found that "search is now a baseline capability".

"Each time a foundation model ships a new feature, another single-purpose app edges closer to the Zero-Value Threshold."

6. The 2×2 Matrix of Absorption Risk

The risk that an AI application will be absorbed by a foundation model breaks down along two axes:

- Verticalization: How specialized is it for a particular industry or domain?

- Technical Complexity: How difficult is it to implement?

These two axes define four zones.

Zone 1: High Risk (Horizontal, Technically Simple)

- Examples: Basic text generation, simple image editing, summarization, generic translation, general-purpose chatbots

- Characteristics:

- High demand and easy to build — foundation models absorb these first and fastest

- Jasper's marketing copy generation is the canonical example

"Jasper's core feature fell squarely in Zone 1, making it easy for foundation models to displace it quickly."

Zone 2: Medium-High Risk (Vertical, Technically Simple)

- Examples: Domain-specific chatbots, industry-specific data extraction, simple workflow builders

- Characteristics:

- Specialized for a particular industry, but technically straightforward

- Once the market grows large enough, foundation models catch up quickly

- Many vertical AI apps fall here

Zone 3: Medium Risk (Horizontal, Technically Complex)

- Examples: Advanced in-IDE code generation, real-time LLM-powered search summarization (Perplexity)

- Characteristics:

- High demand, but difficult to implement — foundation models can't catch up immediately

- Technical complexity serves as a defensive barrier

Zone 4: Low Risk (Vertical, Technically Complex)

- Examples:

- Harvey: legal reasoning with embedded law-firm-specific knowledge

- Hippocratic AI: clinically validated medical voice agents

- Characteristics:

- Proprietary data, complex workflows, and regulatory requirements form strong moats

- Foundation models cannot easily replicate these

"Zone 4 products face high barriers around accuracy, accountability, and regulation, making them difficult for general-purpose LLMs to replace."

7. MCP (Model Context Protocol) and the Shifting Moat

Anthropic's MCP standardizes how foundation models interact with external data, tools, and specialized functionality. Previously, the act of connecting an LLM to external capabilities was itself a moat — but MCP has made "connectivity" no longer a differentiator.

"The real moat now lies in the 'last mile' — complex edge-case handling, regulatory compliance, proprietary data, and deep workflow integration."

8. The Optimal Specialization Range for AI Applications

Traditional SaaS valued larger TAM (Total Addressable Market) as inherently better, but in AI applications, targeting too broad a market actually increases the risk of being absorbed by a foundation model.

- Too broad: Foundation models will catch up soon

- Too narrow: Hard to reach venture scale

- The right level of specialization yields the strongest moat

"AI applications should ideally start narrow and deep, build a moat, and then expand gradually."

9. Vertical Multi-Agent Networks: A New Form of Moat

"If tomorrow's foundation models can replicate any general-purpose capability, the moat must come from depth. That's why we believe vertical multi-agent networks will form powerful moats."

- Characteristics:

- Specialized agents collaborate across each step of a workflow

- Actively integrates with external tools via MCP

- Combines proprietary data, deep workflows, and continuous learning

- Especially powerful in domains where regulation, accuracy, and accountability matter

10. D Factor: The Core of AI Application Valuation

Traditional SaaS valuation (ARR multiples) does not account for the Displacement Risk (D Factor) posed by foundation models.

- D Factor:

- Ranges from 0 to 1

- 0: Strong moat

- 1: Value is already collapsing

"Most AI applications have a D Factor much closer to 1 than their founders realize."

D Factor Assessment Criteria

- Performance gap versus foundation models

- Depth of integration within customer workflows

- Proprietary data network effects

- Regulatory and compliance barriers

Examples:

- ARR $10M, SaaS multiple 10× → $100M valuation

- D Factor 0.9 → Actual value: $10M

- D Factor 0.2 (e.g., medical AI) → Actual value: $80M

"Investors are no longer willing to apply high multiples to companies with a D Factor above 0.9."

11. Four Reasons AI Companies Can Command Higher Valuations Than SaaS

-

Faster growth trajectory

- Many cases can transform entire industries

-

Higher capital efficiency

- Revenue can scale via technology without expanding headcount

-

Higher margins

- Automation and data feedback loops reduce labor costs

-

Shifting business model

- Transition from SaaS (per-seat pricing) to Service-as-Software (outcome-based pricing)

- TAM expands to include the labor cost market

"AI companies can now go after labor budgets — not just software budgets."

However:

"The D Factor must always be considered. High growth and efficiency alone do not guarantee real value."

12. Lessons from the AI SDR Boom

Over the past two years, hundreds of millions of dollars have been invested in AI SDR (sales automation), but most of these companies carry a D Factor of 0.7–0.9 — meaning they are exposed to the risk of losing 90% of their value.

Four Structural Risks

- Thin data moat: Reliance on public data that foundation models can easily replicate

- Low switching costs: Customers churn immediately when performance drops

- Platform bundling: Large software players replicate and bundle the feature

- Declining ROI: When everyone is selling with AI, the effectiveness drops sharply

"If you invest based on ARR alone, the actual value — once D Factor is applied — will be far lower."

13. The Future of AI Applications in the AGI Era

Some fear that:

"Foundation models will soon absorb every application, and application-layer startups will cease to exist."

Indeed, the task-length that AI can handle is doubling every seven months. By 2027, AI is expected to handle full-day tasks; by 2028, full-week tasks.

But the authors argue:

"We do not subscribe to the AI application apocalypse. AGI will actually open new markets. Labor budgets, consulting fees, and professional services are the trillions of dollars in real market opportunity that AI can pursue."

14. The Four Stages of Moat Formation

Moats don't appear overnight. Here are the four stages an AI startup goes through as it builds one:

-

Pre-Moat (Early Stage):

- Ambition is high, but no real moat exists

- Lacking proof of customers, workflow integration, etc.

- Even modest foundation model progress creates immediate displacement risk

-

Moat Construction:

- Paying customers, actual workflow integration

- Partial regulatory approvals, proprietary data, etc.

- Moat is still fragile

-

Moat Validation:

- No customer churn despite major LLM releases

- Moat proven through real retention data

-

Mature Moat:

- Brand, deep integration, exclusive regulatory relationships, etc.

- Premium partnerships, large-scale expansion, and acquisition become possible

- Risk of immediate displacement is greatly reduced

15. Conclusion: Survival Strategies for AI Applications

- Targeting too broad a market risks absorption by foundation models and a value collapse to zero.

- In narrow, deep vertical markets, survival and growth hinge on building moats through:

- Proprietary data

- Complex workflows

- Regulatory and compliance barriers

- Multi-agent networks

"Only companies that continuously innovate within vertical markets, build deep domain expertise, and solve real problems will be able to capture the trillions of dollars in new markets ahead."

Key Terms:

Zero-Value ThresholdFoundation ModelAbsorption RiskD Factor (Displacement Risk)VerticalizationTechnical ComplexityMoatMulti-Agent NetworkMCP (Model Context Protocol)SaaS vs Service-as-SoftwareAGI (Artificial General Intelligence)Four Stages of Moat Formation

😊 If you found this useful, share it with someone thinking about which AI companies will truly survive.