1. Introduction: The Chaos of AI Company Valuation

- OpenAI's valuation differs wildly depending on who you ask: SoftBank says $300B, Microsoft says $157B, and Elon Musk says $97B.

- This extreme divergence in AI company valuations isn't just an OpenAI problem — it reveals a deeper issue: the absence of a systematic framework for evaluating AI companies.

"VCs complain that AI company valuations are too high, yet they offer no alternative method for valuing this new type of company."

- Traditional metrics like ARR (Annual Recurring Revenue) multiples fail to capture AI's unique dynamics — namely, the exponential pace of model improvement and the 'zero-value threshold' (the phenomenon where yesterday's cutting-edge technology becomes worthless today).

- Analogies to cloud computing also have limits. Switching costs between AI API providers are extremely low, meaning these companies have weak "stickiness."

2. The Need for a New AI Valuation Framework

- AI companies are fundamentally different from traditional SaaS — competition and value destruction happen far more rapidly and drastically.

- The traditional valuation formula (Value = ARR × Multiple) assumes gradual market change, but AI companies are exposed to "existential threats" where their reason for existing can vanish overnight.

"Traditional metrics give investors false confidence, because the AI market is defined not by continuity but by discontinuity."

- AI's displacement risk is qualitatively different from the gradual substitution of legacy technologies.

- If a foundation model is caught by open source, its value evaporates instantly.

- AI applications can become meaningless overnight if the foundation model absorbs their functionality.

"In AI, the moment a meaningful technical advantage disappears, enterprise value effectively hits zero. All that remains is talent and infrastructure."

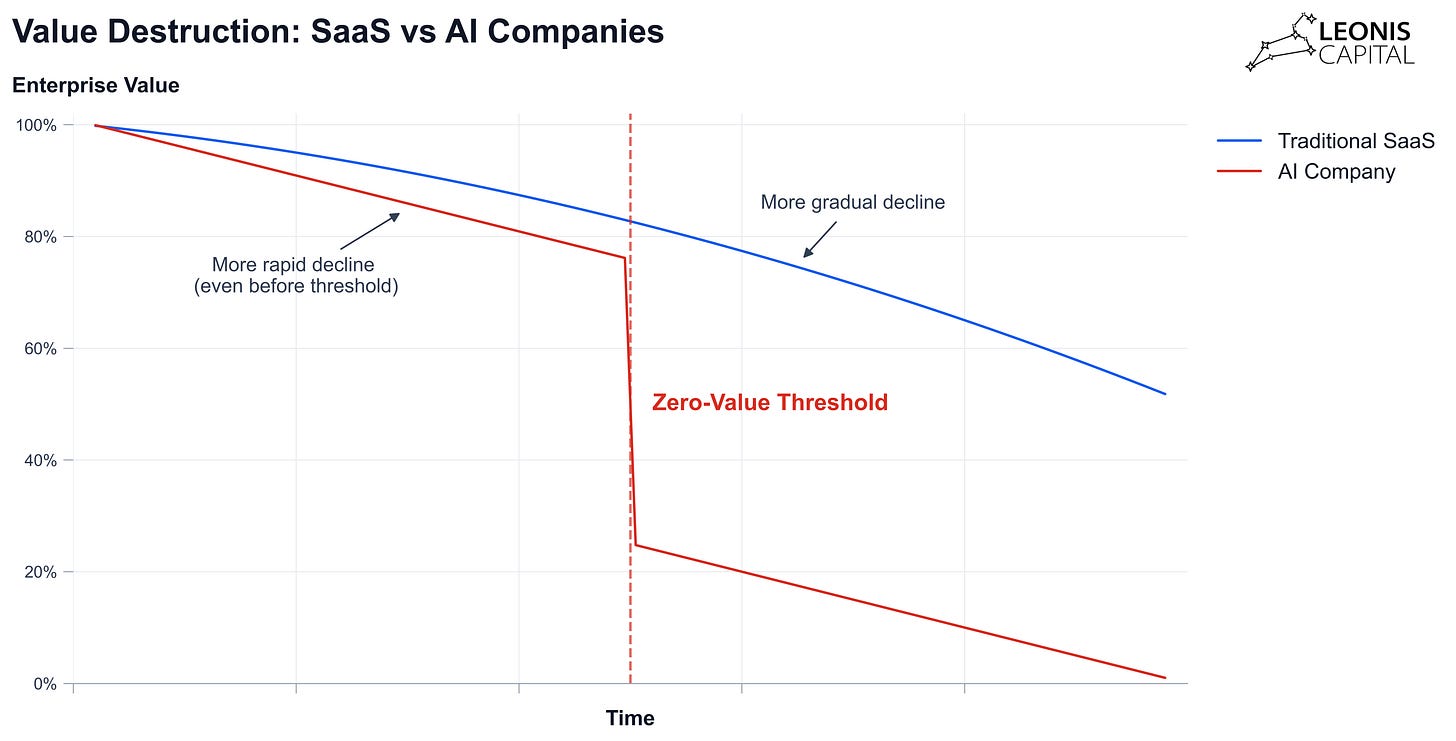

3. The Zero-Value Threshold and AI's Value Destruction Curve

- The zero-value threshold is the point at which:

- A foundation model company's value collapses toward zero the moment it falls behind open-source performance,

- An application company's value collapses toward zero the moment the foundation model replicates its core functionality.

"AI companies are either meaningfully ahead of the threshold, or they face a sharp plunge into value destruction."

- Traditional SaaS experiences gradual customer churn, but AI companies suffer a vertical drop in value the moment the threshold is crossed.

4. The AI Valuation Formula: Introducing the Displacement Risk Factor (D)

- The new formula:

Enterprise Value = ARR × Valuation_Multiple × (1 - D)- D (Displacement Risk Factor): A value between 0 and 1 that quantifies the probability that a company's core value will be displaced.

"The key innovation in this formula is D — the displacement risk factor. This single number makes explicit the risk that a company's value could become zero at any time."

- Foundation model companies:

- D is determined by technical lead over open source, efficiency, and the defensibility of specialized capabilities.

- Application companies:

- D is determined by how easily the foundation model can replicate the functionality, workflow integration depth, network effects, and similar factors.

"Estimating D precisely is difficult, but even a rough estimate forces both investors and management to confront the fundamental question: 'When could this company's value reach zero as AI advances?'"

5. The Open-Source Chase and the "Death Zone"

- Open-source models are catching up to closed models in an average of 5–22 months — and the gap is narrowing.

- When open source catches up in performance, companies see usage drop off a cliff, not gradually.

"The moment open source reaches performance parity, usage decline is not gradual — it's a cliff. We call this interval the 'Death Zone.'"

- The more specialized the domain, the faster open source closes the gap.

- Example: GPQA (PhD-level reasoning) — 5 months; GSM1K (elementary math) — 3–10 months.

6. The Limits of Technical Moats and Estimating Displacement Risk (D)

- Technical moats erode within months due to talent mobility, published papers, and open research.

- When an architectural breakthrough occurs, existing advantages can become irrelevant in an instant.

"Even a revolutionary training technique or architectural breakthrough gives you an edge measured in quarters, not years."

- Example D values:

- Technology leader (6+ months ahead of open source): D = 0.1–0.2

- Marginal advantage (1–3 months): D = 0.3–0.5

- At parity with or behind open source: D = 0.9–1.0

7. Strategies for Escaping the Death Zone — and Their Limits

- Domain specialization (e.g., Cohere)

- Infrastructure pivot (e.g., Stability AI)

- Retreat to the application layer (e.g., Baichuan AI)

"These strategies may help with survival, but measured against the original foundation model vision, they represent a 90% decline in value."

- Conclusion: "If you're not more than six months ahead of open source, you've already entered the Death Zone."

8. Valuing Foundation Model Companies: How It Differs from SaaS

- Unlike SaaS, foundation model companies are:

- Capital-intensive (training costs running into the tens or hundreds of billions)

- Low-stickiness (easy to switch APIs)

- High-variance margins (open source offers equivalent capability for free)

- A model portfolio (holding multiple specialized models) raises switching costs and enables price differentiation and upsell opportunities.

"SaaS's 'Rule of 40' (growth rate + margin > 40%) does not apply to AI. AI companies must demonstrate not just growth and profitability, but capital efficiency and improving unit economics."

9. The Value Cliff Created by the D Factor and Multiple

- The apparent difference between a technology leader (15–20x, D = 0.1–0.2) and a pre-displacement company (10–14x, D = 0.3–0.5) looks small — but the actual valuation gap is enormous.

"A small change in the D factor has an outsized impact on enterprise value. This is why investors are obsessed with OpenAI's technological leadership."

10. Practical Application: Valuing OpenAI and Major Foundation Model Companies

- OpenAI valuation example:

- Bull Case: D = 0.1, Multiple = 20x, Revenue = $11.6B → $208.8B

- Bear Case: D = 0.2, Multiple = 15x, Revenue = $11.6B → $139.2B

"Under our framework, OpenAI's value falls between $139.2B and $208.8B. SoftBank's $300B is too high; Musk's $97B is too low."

- Only 2–3 companies can sustain technology leadership; the rest risk falling into the Death Zone.

- Tier-2 and below companies (Mistral, Cohere, etc.) show extreme divergence between market value and intrinsic value.

11. Conclusion: The Essence of AI Valuation and a Survival Strategy

- An AI company's true value depends on its distance from the Death Zone — that is, on sustainable technological advantage.

- When displacement risk (D) is multiplied against traditional metrics, most AI companies are worth far less than their market valuations imply.

- Strategic pivots are not optional — they are a matter of survival.

"This is not pessimism; it is strategic clarity. The only unforgivable mistake in the AI ecosystem is misunderstanding the fundamental dynamics that determine whether your company becomes zero — or a hero."

12. Coming Up Next

- Part II will apply the same framework to AI application companies, analyzing which categories will survive and which are destined to be absorbed by foundation models.

Key Concept Summary

- Zero-Value Threshold

- Displacement Risk (D)

- Foundation Models vs. Open Source

- Death Zone

- Collapse of the Technical Moat

- Differences Between SaaS and AI Company Valuation

- Model Portfolio Strategy

- Divergence Between Market Value and Intrinsic Value

- Strategic Pivots for Survival

- The Conditions for Sustainable Value in AI Companies

😊 If you found this analysis helpful, please share it with others! Stay tuned for Part II, where we'll go even deeper.